Fintech compliance in Canada has become increasingly complex in recent years. With evolving anti-money laundering (AML) regulations and heightened oversight by FINTRAC, many money service businesses (MSBs) and payment service providers (PSPs) are struggling to keep up.

Each regulatory update brings new obligations that you must interpret and implement correctly, making compliance challenging. Without expert guidance, these rules can quickly become overwhelming. That’s why working with a specialized fintech law firm is crucial. If you wish to learn more, continue reading.

What is Fintech Compliance in Canada?

Fintech compliance refers to how financial technology companies follow the legal and regulatory standards set by authorities such as FINTRAC, Revenu Quebec, and the Bank of Canada. These standards have been designed to detect and prevent financial crimes such as:

- Money laundering

- Terrorist activity financing

- Sanctions evasion

Any company that doesn’t adhere to fintech regulations and engage in financial crimes will be subject to penalties. These may be minor fines, administrative monetary penalties (AMPs), public disclosure, and/or imprisonment.

Why New AML Regulations Make Fintech Compliance Challenging?

Canada’s regulatory landscape is constantly evolving to adapt to the changing times and financial technology. Key factors that make fintech compliance with new AML regulations challenging include:

Regulatory Complexity

The regulatory framework for fintech is multi-layered. A single company may need to comply with federal requirements under FINTRAC, provincial regulations such as Revenu Quebec licensing for MSBs, and industry-specific expectations from the Bank of Canada for PSPs.

Resource Constraints

Most fintech businesses operate with a limited budget, especially during the initial stages. Appointing full-time compliance officers and maintaining physical presence in Canada to fulfil FINTRAC MSB compliance office requirements are costly conditions that many businesses are not able to afford.

Increased Scrutiny

FINTRAC has increased audits and enforcement since 2022. Businesses that fail to maintain proper AML compliance may face AMPs, public naming on FINTRAC’s violation list, or license suspension.

How A Fintech Law Firm Can Help You Navigate AML Compliance?

Navigating Canada’s ever-changing regulatory landscape is easier with a skilled fintech lawyer by your side. Firms such as Renno Co. & Fintech can assist you in the following ways:

- Comprehensive Internal Review

A fintech compliance professional can review your business’s internal anti-money laundering program. They will identify weaknesses within your policies and suggest amendments that can strengthen your AML program.

Law firms also help fulfil obligations such as conducting AML effectiveness reviews or audits every two years to address deficiencies that may exist in your MSB's compliance programs. Once internal weaknesses are addressed, the next step is developing stronger AML policies.

- AML Policy Drafting and Implementation

FINTRAC, Bank of Canada, and Revenu Quebec require MSBs and PSPs to have strong know-your-customer (KYC) policies and risk management frameworks. A legal expert can assist you by developing compliance manuals and risk templates tailored to your business model.

They can also assess your business’s internal AML program to identify gaps, outdated procedures, or areas of non-compliance. A fintech law firm’s guidance strengthens your compliance structure and reduces the risk of penalties or regulatory scrutiny.

- MSB or PSP Employee Training

Training employees is essential for meeting reporting requirements set by FINTRAC, such as:

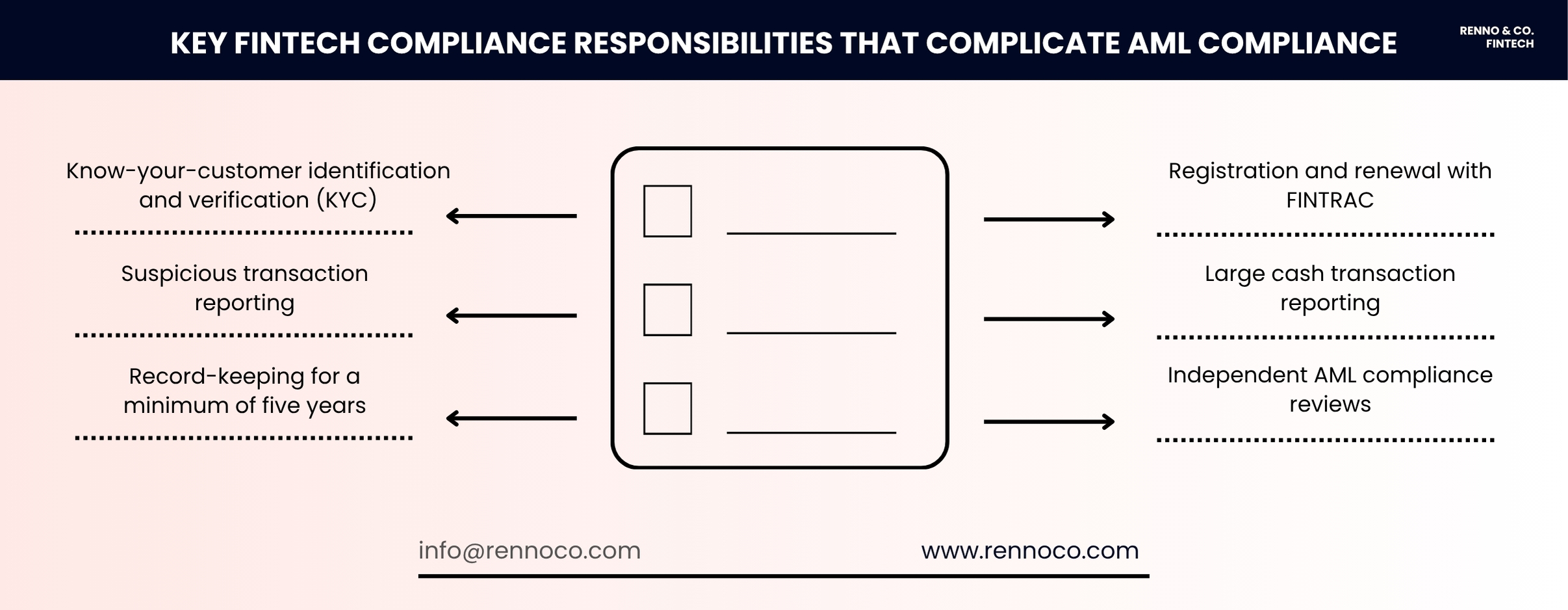

- Suspicious transaction reporting

- Large cash transaction reporting

- Electronic funds transfer reporting

- Large virtual currency transaction reporting

An industry-leading law firm can conduct training sessions to enhance your team’s ability to identify unusual transactions and report them properly.

- FINTRAC Regulatory Representation

If your company is audited for non-compliance, FINTRAC may require an in-person meeting with your designated compliance officer. This role is legally responsible for developing and maintaining your AML program. A fintech law firm such as Renno Co. & Fintech can provide fractional AML services to help you meet these obligations.

This includes offering a Canadian-based representative and private office to establish the required physical presence in Canada. These resources ensure your MSB remains compliant and audit-ready, while satisfying both FINTRAC expectations and banking partner requirements.

- Ongoing Monitoring and AML Updates

A fintech law firm continuously equips itself with the latest AML regulation knowledge in Canada by monitoring FINTRAC and Bank of Canada updates. They help you keep up with the ever-changing laws and implement new anti-money laundering policies.

With strong legal support, your company will never be behind in fintech compliance. You will also not have to worry about facing penalties due to FINTRAC non-compliance.

FAQs

Is Fintech Compliance in Canada Mandatory?

Yes, fintech compliance is mandatory if you’re a money service business or payment service provider in the country. As long as your services fall under the scope of FINTRAC, Bank of Canada, or Revenu Quebec, you must ensure strict compliance.

Why is AML Compliance Important for MSBs and PSPs?

AML compliance protects companies from unintentionally facilitating financial crimes such as money laundering in Canada. It holds companies accountable for not reporting suspicious transactions through heavy fines, public disclosure, or imprisonment.

What are FINTRAC’s Main AML Obligations?

FINTRAC’s main anti-money laundering obligations include reporting of suspicious transactions, verification of client identities, and maintaining business records for at least five years.

How can You Improve FINTRAC Compliance in Canada?

You can enhance FINTRAC compliance by conducting an AML effectiveness review every two years. The internal analysis will help you identify gaps within your compliance program and implement new policies to correct those deficiencies.

Ensure Fintech Compliance With New AML Regulations With Renno Co. & Fintech

Fintech compliance under Canada’s new AML regulations is challenging, but not impossible. With complex laws, evolving technology, and growing FINTRAC oversight, expert legal support is essential. Otherwise, you may risk losing your business license or reputation.

A fintech law firm like Renno Co. & Fintech helps your business stay compliant and confident in a rapidly changing environment. We assist businesses with MSB and RPAA registrations, AML audits, outsourcing of compliance officers, & more. Contact us today if you’d like to speak to one of our fintech compliance advisors.