All money service businesses (MSBs) and fintechs registered with FINTRAC must perform periodic AML effectiveness review. It is a legal requirement that banking providers and other regulatory agents want you to fulfill.

As a new MSB, you may not know what an AML effectiveness review assesses. Let’s look at what is expected from your MSB and how we can help you.

What is an AML Effectiveness Review?

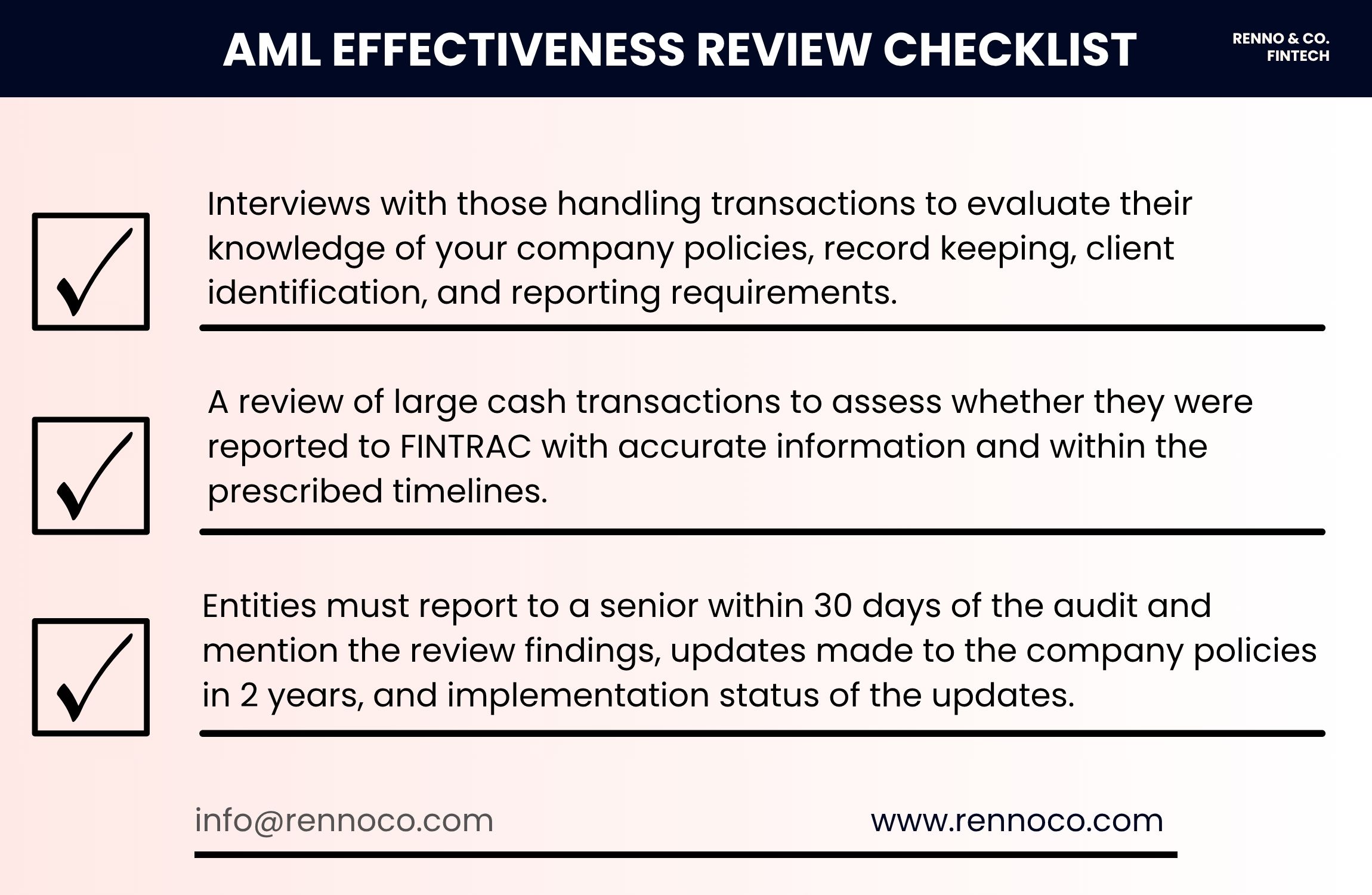

An AML effectiveness review (also referred to as an AML audit) is a full-scope review of your anti-money laundering compliance program. It evaluates whether your policies, controls, and procedures are documented and working in practice.

Under Canadian law, every FINTRAC-regulated entity must complete an effectiveness review every two years. You should start the audit no later than 24 months after the last AML review.

Why is an AML Audit So Important?

An effectiveness review is the tool that:

- Verifies your AML/CTF program is performing as designed

- Identifies gaps or blind spots in your controls

- Assures regulators and banking partners

It allows you to identify weaknesses of your MSB’s compliance program and fix the gaps before authorities take action. Failing to conduct a timely audit and strengthen your compliance policies allows FINTRAC to enforce punishment.

You may face monetary penalties, criminal liability, bank account closures, and more.

What FINTRAC Expects from Your AML Audit

Whenever FINTRAC examines a MSB, it asks for the latest AML effectiveness review report. The regulatory agency expects you:

- Conduct an audit every two years as designated

- Get the review completed by an independent party

- Cover all five pillars of the compliance program

If you provide no report or outdated findings, the agency has full authority to take action.

What Banks Expect from Your AML Audit

Banking providers always request a copy of the latest AML audit when onboarding a MSB. They’ll consider your application incomplete if no review report is attached.

You’re expected to develop a comprehensive document containing the findings of the last AML review. Banks also expect you to get the audit done by an individual who understands Canadian fintech laws thoroughly.

If you cannot meet these expectations, getting banked in Canada will be difficult. This is especially true if you want to onboard a big 5 Canadian bank.

Renno Co. & Fintech’s AML Effectiveness Review: What we Deliver

The AML audit is a 360 review of your company's AML compliance function. When you contact us for your AML effectiveness review, we follow a detailed process that is fully aligned with FINTRAC and banking expectations:

- Policy & Program Review

We examine your written policies and procedures to ensure they:

- Align with current laws and FINTRAC guidance

- Reflect your actual business activities

- Include procedures for identifying and reporting suspicious transactions

Our legal advisors always keep up with the latest fintech regulations to ensure your documents are accurate.

- Risk Assessment Validation

All MSBs must use a risk-based approach for AML audits. We review your measures to confirm:

- Risk categories are properly identified (client, product, delivery channel, geography)

- Ratings are logical and based on clear criteria

- Controls are tied to your inherent risk profile

The main purpose of risk validation is to ensure your business is not flagged by FINTRAC and banks later.

- Compliance Training Evaluation

FINTRAC and Canadian banks want your MSB to have a robust compliance program. The program must also include training measures for staff. Our officers will evaluate this aspect of your compliance program to ensure:

- Training is up to date and role-specific

- Staff understand reporting obligations and red flags

- Training records are complete and verifiable

Having a compliance program is not enough unless all members of the company participate in maintaining the rules.

- Review of Ongoing Monitoring & Reporting

Renno Co. & Fintech’s advisors evaluate:

- Your processes for filing suspicious transaction reports, large cash transaction reports, and large virtual currency transaction reports

- How do you identify unusual or suspicious activity

- Whether monitoring is documented and reviewed

With this step, we’ll determine whether your business is complying with FINTRAC’s monitoring and reporting obligations.

- Recordkeeping and Data Controls

Businesses are expected to meet recordkeeping obligations by FINTRAC. That’s why we:

- Examine the retention of KYC files

- Record storage protocols

- Access controls and security measures

Evaluating this data assists in determining any recordkeeping violations.

- Governance & Oversight Checks

The final step of an AML effectiveness review involves oversight checks. We evaluate whether:

- The compliance officer is properly empowered and resourced

- Management is receiving reports and responding to risks

- Board-level oversight is documented where applicable

After completing the check, we’ll compile all the findings of the AML audit in a single report.

What’s in the Final AML Audit Report?

After conducting the AML effectiveness review, we will provide you with a report which will:

- Satisfy Your Regulatory Requirements

- Maintain Banking Relationships

- Provide Actionable Recommendations

Our report provides a tailored and detailed summary of findings with actionable insights on how to improve the AML function of your business to meet industry best practices.

Common Issues We Flag in Our AML Effectiveness Reviews

Our audit review allows you to strengthen your compliance policies to avoid AML red flags. Here are some of the most common gaps we find and help fix:

- Outdated policies that don’t reflect recent regulatory changes

- Risk assessments that don’t address real exposure (e.g., crypto, cross-border clients)

- Training logs that are incomplete or inconsistent

- Weak monitoring protocols (e.g., no alerting thresholds, no documentation)

- Missing audit trails for transaction review or escalations

- KYC records missing key ID verification steps

A Strong AML Audit Keeps You Compliant: Work With Us For Your Biennial Review

All FINTRAC MSBs and registered businesses must complete an AML effectiveness review every two years. It is a legal requirement and business necessity that helps your MSB stay safe.

Renno Co. & Fintech delivers tailored, regulator-ready AML audits that help your business stay compliant, grow faster, and earn the trust of regulators and banks.

Contact us today to schedule your AML effectiveness review and receive an audit that actually delivers value.