The evolving financial sector in Canada requires businesses to follow strict FINTRAC regulations. These rules also apply to all products and services launched by financial companies, including fintech apps. If your Fintech App is found to be non-compliant with FINTRAC, you may be subject to severe consequences that may affect your overall business operations, professional reputation and personal life.

If you’re wondering about what the consequences can be if your fintech app is non-compliant with Canadian regulations, you’ve come to the right place. This article will cover Canadian fintech app compliance requirements and consequences for failure to comply.

What is a Fintech App?

Money service businesses (MSBs), payment service providers (PSPs), crypto exchanges, and other types of entities can assist consumers with financial services. Fintech apps are solutions launched by companies to help customers make seamless money transfers, readily purchase cryptocurrency, and more.

You may also launch a fintech app in Canada to help customers view all your products and services in one place. Businesses mainly offer fintech applications to provide efficiency, accessibility, and convenience to consumers.

What are Fintech App Compliance Requirements?

All fintech apps must ensure compliance with regulatory frameworks in Canada. The Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA) governs MSBs, PSPs, and other companies involved in offering money services.

It also governs fintech apps launched by any of these companies to reduce the rate of financial crimes. FINTRAC is the organization that ensures companies follow regulations under the PCMLTFA. This is why you must meet fintech app compliance requirements, such as:

- Verifying user identity before allowing financial transactions

- Reporting suspicious or large-value transactions

- Keeping detailed financial records for at least five years

- Registering with FINTRAC before beginning business operations

Even if your fintech application is fully digital, it falls under the same scrutiny as a brick-and-mortar Canadian MSB.

Top 5 Examples of a Non-Compliant Fintech App

Non-compliance occurs when a fintech app fails to meet any of the obligations under the (PCMLTFA). This could include:

- A fintech app without MSB registration, RPAA registration, or Revenu Quebec registration, leading to illegal operations

- An app that doesn’t report suspicious transactions under FINTRAC regulations, leading to FINTRAC non-compliance

- Fintech apps with inadequate client identification processes, leading to non-compliance with know-your-customer (KYC) requirements

- A loan lending fintech application that doesn’t store records for at least five years, as required by FINTRAC

- Fintech apps with outdated anti-money laundering (AML) policies

By operating a non-compliant fintech app, you will be violating FINTRAC regulations. The organization will be required to address the non-compliance under the PCMLTFA.

How Does FINTRAC Address Non-Compliance?

When a fintech app is non-compliant with FINTRAC regulations, the agency can address the violation in various ways. These include:

- Take no action

- Perform a follow-up compliance assessment

- Implement an administrative monetary penalty (AMP)

- FINTRAC non-compliance disclosure

The extent of FINTRAC non-compliance mainly determines the type of action the agency takes against a business.

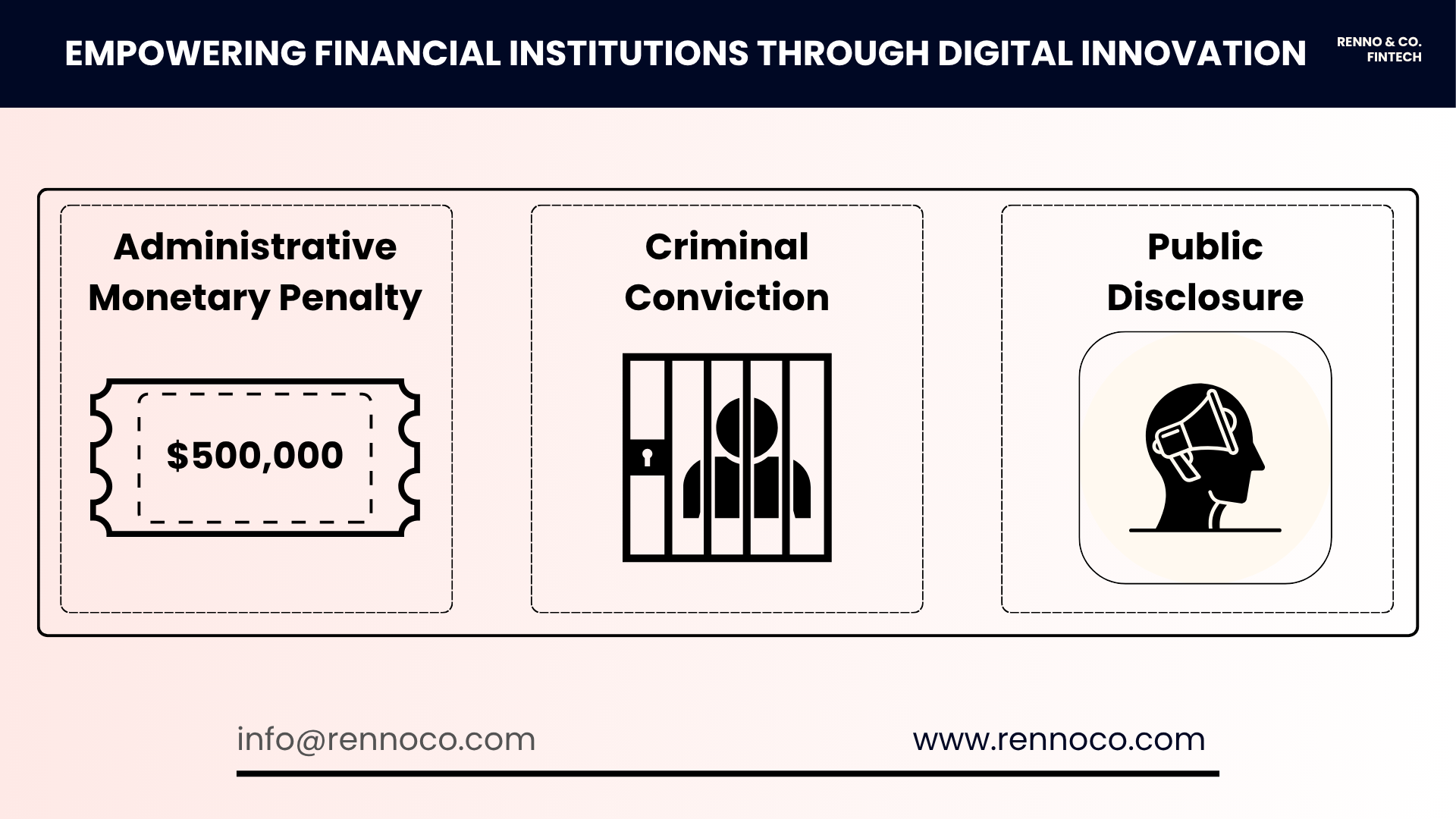

What Will Happen if Your Fintech App is Non-Compliant with FINTRAC Regulations?

If FINTRAC decide to take action against your non-compliant fintech app, it may be:

1. Administrative Monetary Penalty

The organization can issue an administrative monetary penalty if it has confirmed that the fintech app has violated the PCMLTFA. These violations can range from minor to very serious, depending on the degree of non-compliance:

- Minor violation - $1 to $1,000

- Serious violation - $1 to $100,000

- Very serious violation - $1 to $500,000

The values may soon increase to $40,000, $4 million, and $20 million or 3% of global revenue (whichever is lower) for minor, serious, and very serious violations, respectively. These 40-fold AMP increases have been suggested by Bill 2C, which may be passed in October 2025.

2. FINTRAC Non-Compliance Disclosure

If a fintech app commits a criminal offence, the organization may provide a FINTRAC non-compliance disclosure. This means they’ll reveal specific information about their compliance assessment to a law enforcement agency or prosecutor for legal action. The consequences of FINTRAC non-compliance disclosure may be a summary or indictable conviction.

Summary Conviction

A non-compliant fintech app will receive a summary conviction if the violation is less severe. The Canadian court may impose a fine of $250,000 or $1 million for FINTRAC non-compliance. They may also supplement the punishment with an imprisonment sentence not exceeding two years.

Indictable Offence

If your fintech app commits a major criminal non-compliance offence, you’ll be subjected to an indictable offence punishment. A fine of up to $2 million may be imposed, with a maximum imprisonment sentence of five years in Canada.

3. Harm Done Violation Penalty

Harm refers to the degree to which non-compliance interferes with the goals of the PCMLTFA under FINTRAC’s harm done assessment framework. When a fintech app fails to verify client identity or beneficial ownership, it enables anonymous transactions that can conceal money laundering or terrorist financing activities.

Such violations weaken Canada’s AML regime and hinder law enforcement investigations. Depending on severity, penalties range from $1 to $1,000 for minor harm done offences and $1 to $100,000 for serious harm done violations.

The Long-Term Impact of Failure to Meet Fintech App Compliance Requirements

The financial and legal risks are significant, but the long-term consequences of failing to meet fintech app compliance requirements can be even more damaging:

1. Loss of Investor Confidence

Investors in fintech rely on transparent risk management and governance. A FINTRAC investigation or public penalty can lead to withdrawn funding or reduced valuations.

2. App Store and Partner Restrictions

Payment processors and app stores (such as Google Play and Apple App Store) can suspend or remove fintech apps associated with non-compliance with new FINTRAC regulations.

3. Customer Trust Erosion

Users expect financial platforms to protect their data and follow legal frameworks. Non-compliance signals negligence, which can cause massive customer loss.

4. Increased FINTRAC Audit Frequency

Once flagged, your fintech app may face more frequent FINTRAC audits or compliance monitoring, diverting resources from innovation and product development.

How to Maintain Fintech App Compliance in Canada?

Maintaining fintech app compliance requires more than meeting technical requirements. It demands continuous oversight and expert interpretation of the PCMLTFA. From registering your business on the FINTRAC list of MSBs in Canada to automating KYC verification, every process must align with evolving regulatory standards.

Recordkeeping, accurate reporting, and regular AML effectiveness reviews are essential to prevent penalties and reputational damage. Navigating these obligations can be complex, especially for startups or international payment providers.

Partnering with professionals like Renno Co. & Fintech ensures your systems, staff training, and reporting practices fully satisfy fintech app compliance requirements. We help your business operate confidently within Canada’s regulatory framework.

FAQs

Are Fintechs regulated in Canada?

Yes, Canadian fintechs are regulated under FINTRAC and the PCMLTFA, requiring registration, client verification, transaction reporting, and strict anti–money laundering compliance measures to operate legally.

What is Fintech Compliance?

Fintech compliance involves following FINTRAC regulations, maintaining AML programs, verifying customers, and reporting suspicious transactions. It encourages secure and transparent financial operations within Canada’s regulatory framework for fintech businesses.

Can I go to Jail for Fintech App Non-Compliance?

Yes, severe or intentional violations of FINTRAC regulations may lead to criminal prosecution, fines exceeding $2 million, and imprisonment of up to five years under the PCMLTFA.

How to Build a Compliant Fintech App?

Develop strong AML programs, automate KYC verification, maintain detailed records, and consult experts like Renno Co. & Fintech to meet all Canadian fintech app compliance requirements effectively.

Collaborate with Renno Co. & Fintech for Effective Fintech App Compliance

FINTRAC compliance isn’t optional but necessary for Canadian money service businesses and payment service providers. A non-compliant fintech app risks fines, legal penalties, and long-term damage to its reputation.

By understanding and applying fintech app compliance requirements, you safeguard your interests. If you need support navigating new FINTRAC regulations, Renno Co. & Fintech offers expert legal guidance tailored to MSBs, PSPs, and other fintech platforms across Canada. Contact us today to schedule a meeting with one of our legal advisors.