Majority of money service businesses (MSBs) in Canada are required to get an RPAA registration in addition to their FINTRAC license in order to provide custodial services. The new Retail Payment Activities Act (RPAA) offers complete details on holding of funds.

Equipping yourself with the latest policies of RPAA will help you follow the rules surrounding custodial services. The good news is you don’t have to look far. We’ll help you understand all about the custodial services you can offer under the RPAA.

What Are Custodial Services in Finance?

Custodial services in finance refer to the safekeeping and holding of securities such as:

- Stocks and equities

- Bonds

- Notes

- Documents that represent a company’s debt owed

- Warrants that indicate a share in a company

As a custodian, you must safeguard securities, process the sale of securities, and adhere to compliance regulations.

What Custodial Services for MSBs Are Allowed Under the RPAA?

A MSB offering custodial services in Canada has to register under the RPAA and follow its rules. This means you can only hold and manage client securities that are allowed under this act.

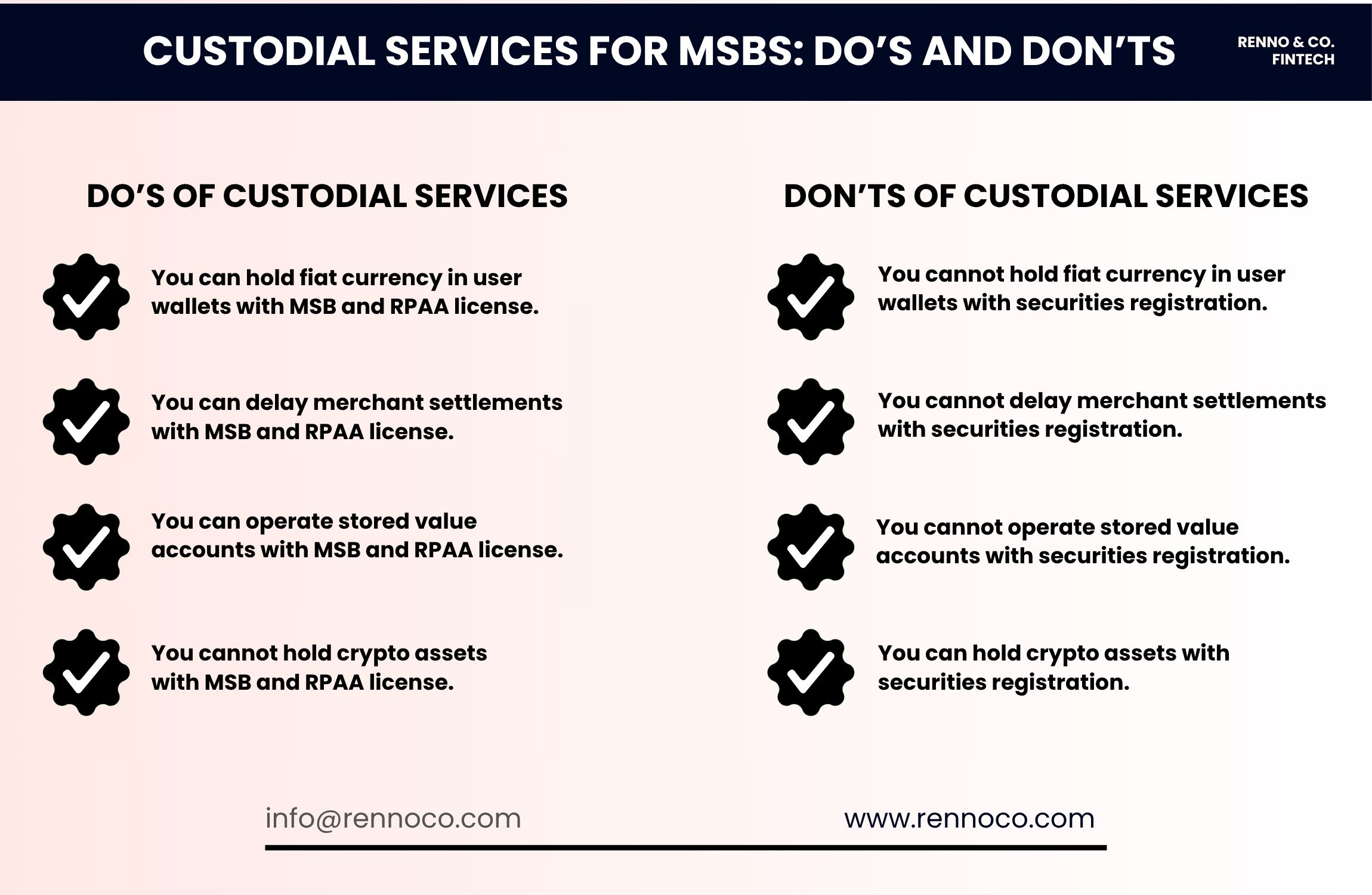

The only allowed custodial services under the RPAA concern fiat currency such as CAD, USD, EUR, and more. You can operate:

- Prepaid wallets

- Account-based remittance systems

- Merchant settlement platforms

- Stored value payment ecosystems

Keep in mind you’ll only be allowed to operate these services if you have a FINTRAC MSB license and RPAA registration approval. Having both licenses will ensure you can hold end-user funds, process payments, and retain balances indefinitely.

What Custodial Services for MSBs Are Not Allowed Under the RPAA?

Holding and processing of crypto assets are not allowed under custodial services for MSBs. The RPAA has strict policies against custody of a client’s cryptocurrency.

If you want to hold Bitcoin, Ethereum, or other digital currencies for clients, you must get additional licenses. You can seek such a license from provincial securities regulators by registering as a restricted dealer

The Canadian Securities Administrators streamline the process of getting additional licenses for crypto assets custody. The Regulatory team at Renno can help with this as well! Contact us for more information.

Why Custodial Services for MSBs Are Tightly Regulated in Canada?

The collapse of FTX4 and other cryptocurrency exchanges has led to tighter custodial services regulations in Canada. Strict measures are being taken to ensure:

- Protection of End-User Funds

Canadian regulatory authorities mandate segregation of funds from business operating capital. They require holding of funds in safeguarded accounts by qualified financial institutions. These strict measures have been design to ensure consumers don’t lose their funds because of custodial service providers.

- To Avoid Security Breaches

Mandatory multi-signature authentication, cold storage requirements, and comprehensive cybersecurity protocols safeguard digital assets against theft. Regulatory agencies also specify minimum standards for encryption, access controls, and incident response planning.

- Access to Funds Even in Operational Insolvency

MSBs must maintain specific reserve ratios and undergo testing to show that client funds will be accessible even in cases of business failure. The RPAA also requires a clear document of recovery plans in cases of operational insolvency.

How to Custody Fiat Currency Under the RPAA?

If you want to custody fiat currency for your clients under the RPAA, you must show the Bank of Canada:

- Details of Safeguarded Accounts

A safeguarded account is a bank account that can be used by MSBs or PSPS to hold end-user funds. Such an account is only designed for custody funds and not for other purposes.

You must get a safeguarded account from a qualified banking partner in Canada. Specific details must also be disclosed to the Bank of Canada, such as:

- The name and location of the financial institution where fiat money is being held

- Confirmatory documents to prove that the safeguarded account is separate from operational funds

Providing this information to the Bank of Canada is essential for RPAA compliance.

- Your Risk Management Framework

All PSPs and MSBs offering custodial services under the RPAA must establish a risk management framework (RMF). If you don’t have a RMF before September 2025, you’ll risk losing your Retail Payment Activities Act license.

Your risk management framework must address:

- Fund flow mapping

- Reconciliation processes

- Backup payment systems

- Business continuity and recovery procedures

Consulting a fintech law firm can help you develop a robust framework to avoid RPAA registration challenges.

- Recordkeeping and Reporting Transparency

The final step of ensuring you can hold fiat money for your clients is complying with recordkeeping and reporting obligations. You must track client balances daily and develop a plan for incident responses.

Meeting this last checkpoint will mean that your MSB is ready to act as a custodian for clients.

Can You Custody Funds Without FINTRAC MSB License or RPAA Registration?

If your MSB holds end-user funds without RPAA registration, you’re in breach of Canadian law. The consequences of which include:

- Denial of registration when enforcement begins

- Regulatory enforcement or penalties by the Bank of Canada

- Banking de-risking, where financial institutions refuse to onboard or maintain your accounts

- Potential criminal exposure if fraud or insolvency arises

Even if you are fully FINTRAC-registered, holding client balances without RPAA registration is not permitted.

Enhance Custodial Services Compliance by Getting Registered First: Contact Renno Co. & Fintech

Navigating compliance measures for custodial services alone can be difficult. This is especially true if you don’t have the latest news on FINTRAC MSB license and RPAA regulations.

Renno Co. & Fintech can help you avoid the struggle of getting a Canadian fintech license. Our lawyers have years of experience in helping clients get MSB registration and RPAA registration approvals.

Book an appointment today to start your fintech registration processes before offering custodial services.